Cost of car insurance: How do I lower my car insurance costs?

Rising cost of car insurance

FOX LOCAL Host Ariyl Onstott and Atlanta insurance broker John D'Angelo explore why car insurance costs are on the rise.

ATLANTA - Has your car insurance cost increased recently? If so, you are not alone—and it’s probably not your fault.

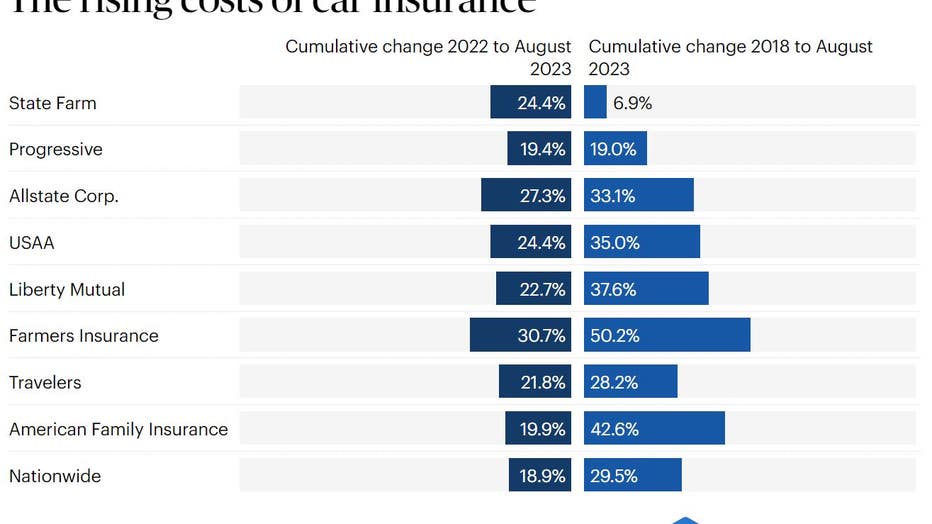

We recently asked our Facebook followers if they had noticed a rise in their car insurance premiums, and nearly 2,000 people responded with a resounding "yes." For the vast majority of these individuals, nothing had changed—they hadn’t bought a new car, been in an accident, received a traffic ticket, added anyone to their policy, or moved. Yet, FOX 5 viewers reported that their rates had increased by 10% to 30%, and in some cases, even more.

With so many people experiencing these unexpected hikes, we decided to take a closer look at what’s happening with car insurance and see if we could uncover some answers.

READ ALL THE STORIES

- Cost of car insurance: Why has car insurance gone up so much in Georgia?

- Cost of car insurance: How do I lower my car insurance costs?

- Cost of car insurance: What drivers can and can't control

- Cost of car insurance: Atlanta vs. everywhere else, it makes a difference

Fortunately, there are a few things that drivers can do to lower the cost of car insurance.

Strategies to lower cost

Here’s a comprehensive list of strategies to save money on car insurance:

1. Shop Around

- Compare quotes from multiple insurers to find the best rate. However, drivers shouldn't simply choose the cheapest – it could be a serious mistake. Larger car insurance companies are generally more financially stable, ensuring reliable claims payouts and coverage during widespread disasters. Big insurers also provide a wider range of policy options, discounts, and extensive service networks, making it easier to access necessary services. Additionally, they often have better customer support and a stronger reputation, which can lead to a smoother, more trustworthy insurance experience.

2. Bundle Policies

- Combine car insurance with other policies (e.g., home, renters) for a multi-policy discount.

3. Increase Deductibles

- Opt for a higher deductible to lower your premium, but ensure you can afford it in case of a claim.

4. Maintain a Clean Driving Record

- Avoid crashes/collisions and traffic violations to qualify for safe driver discounts.

5. Take Advantage of Discounts

- Ask about discounts for things like being a good student, low mileage, anti-theft devices, and defensive driving courses. Better yet, drivers should ask insurance companies for a list of ALL the discounts that are available. Insurance companies don't necessarily know what individual drivers may be eligible for.

6. Don't pay for insurance you may not need

- Liability-only insurance is commonly available for older, lower-value cars where full coverage isn't cost-effective. This type of insurance is often chosen for paid-off vehicles, less frequently driven cars, or those that aren't essential for daily use. Georgia law requires minimum liability coverage of $25,000 per person and $50,000 per accident for bodily injury, and $25,000 for property damage.

7. Consider Usage-Based Insurance

- Pay-per-mile or telematics-based insurance can lower costs for low-mileage drivers. Allstate, Geico, Nationwide, Progressive, Root and State Farm all have usage-based insurance options. However, they may not volunteer this information. Click here for the other options offered by the larger insurance companies.

8. Review Your Coverage

- Drivers should periodically review their policies and adjust overage based on current needs. Drop unnecessary coverage on older vehicles or vehicles that are not driven often.

9. Improve Your Credit Score

- Insurers often use credit scores to determine rates. Drivers with higher credit scores will generally receive better rates than drivers with low credit scores. The average nationwide cost for full coverage for someone who has poor credit is $4,338 for full coverage insurance — $1,795 more than drivers with excellent credit with the same level of coverage.

10. Limit Claims

- Avoid making small claims to keep premiums from rising due to frequent claims. It could be wiser to pay out of pocket to fix small dents and damage or to just live with it if it does not affect the performance and safety of the vehicle.

11. Ask About Group Insurance

- Some employers or organizations offer group insurance rates that are lower than individual rates.

12. Keep Continuous Coverage

- Avoid lapses in coverage, as insurers often charge higher rates for those who have had a gap in insurance.

13. Consider Paying Annually

- Paying your premium in full annually rather than monthly can sometimes result in a discount.

14. Use a Loyalty Discount

- Some insurers offer discounts for staying with them for a certain number of years.

15. Limit Optional Coverages

- Consider whether you need extras like roadside assistance or rental car coverage. AT&T, Verizon and T-Mobile offer roadside assistance to their customers. Rental car coverage is not essential for everyone. Consider the cost versus out-of-pocket rental expenses and the likelihood of needing it, based on driving habits, area, and access to another vehicle or public transportation.

16. Review Your Mileage

- Report accurate mileage; driving less can lead to lower premiums. Drivers who do not drive daily or have very short commutes could qualify for lower rates.

17. Ask About Affiliation Discounts

- Professional associations, alumni groups, or other organizations may offer insurance discounts.

18. Consider the Impact of Adding Drivers

- Adding younger or high-risk drivers to your policy can increase your premium significantly. Ask the younger or high-risk driver to help with the expense as much as possible. If they are unable to do so, decide if they truly need a vehicle or can rely on other transportation.

19. Regularly Review and Compare

- Even if you’re happy with your current insurer, compare rates every couple of years to ensure you’re still getting the best deal. Keep in mind that most insurance companies view it as a negative if a customer often changes companies.

Insurance companies with competitive rates

Here is a list of car insurance companies often recognized for offering competitive rates:

- Geico: Known for consistently low rates and numerous discounts.

- State Farm: Offers competitive rates, especially for young drivers and those with good driving records.

- USAA: Provides excellent rates but is only available to military members, veterans, and their families.

- Progressive: Competitive pricing with options like the Name Your Price tool.

- Liberty Mutual: Offers advantages to drivers who want to work with a local agent or bundle coverage.

- Nationwide: Offers good rates, especially for bundling policies.

- Farmers Insurance: Provides competitive rates with various discount options.

Most expensive vehicles to insure

Here is a list of vehicles that are generally more expensive to insure due to factors like high repair costs, luxury status, or performance capabilities:

- Tesla Model S: High repair costs and advanced technology.

- BMW i8: Luxury hybrid sports car with expensive parts.

- Porsche 911: High-performance sports car with costly repairs.

- Mercedes-Benz S-Class: Luxury sedan with expensive components.

- Audi R8: High-performance sports car with high repair costs.

- Maserati Quattroporte: Luxury vehicle with expensive parts and repairs.

- Ford Mustang GT: Performance vehicle often driven at high speeds.

Least expensive vehicles to insure

Here’s a list of modern vehicles that are generally the least expensive to insure due to their strong safety features, low repair costs, and overall reliability:

- Subaru Outback: Known for safety and reliability.

- Honda CR-V: Popular compact SUV with affordable insurance.

- Mazda CX-5: Offers good safety ratings and low insurance costs.

- Toyota RAV4: Reliable and inexpensive to insure.

- Honda Civic: Compact car with affordable insurance rates.

- Toyota Camry: Mid-size sedan known for safety and low insurance costs.

- Hyundai Tucson: Compact SUV with competitive insurance rates.

What about specialized insurance policies?

Sometimes, drivers can lower car insurance costs for expensive cars by opting for specialized insurance policies. Options like agreed value policies ensure the driver is compensated based on a pre-agreed value rather than a depreciated one, which can be beneficial for high-value vehicles. Usage-based insurance, which charges premiums based on how much you drive, can also save money if the expensive car is used infrequently.

Additionally, specialized insurers may offer discounts for bundling policies or installing advanced security systems. If a car is a classic or collectible, you might qualify for collector car insurance, which typically has lower premiums due to limited driving and better maintenance.

Is it better for drivers to do the shopping or use an insurance broker?

Shopping for your own car insurance allows you to directly compare quotes and choose the best option, offering transparency and full control over the process. However, it can be time-consuming and might limit access to certain policies that are only available through brokers.

On the other hand, using an insurance broker can save you time by handling the comparison for drivers and providing expert advice. They also have access to far more insurance carriers than the regular driver is aware of. Brokers often have access to a wider range of policies, but their recommendations may be influenced by commissions, and there may be additional fees.

Do drivers have to buy car insurance from a company?

There are a few states that do not require a driver to have car insurance purchased through an insurance company, including the state of Georgia. The states consider it "self-insurance" and they require pretty steep amounts of money to be available if the driver needs it for a crash.

Each state has an approval process and requires the funds to be held separately from your personal finances so they are available immediately if needed. The driver is also required to handle the situation in a similar manner as an insurance company and any paperwork and legal proceedings are the driver's responsibility.

The states are California, Connecticut, Florida, Georgia, Hawaii, North Dakota, Pennsylvania and Vermont.

In Georgia, a driver must have a $50,000 surety bond or security deposit and $100,000 net work. Click here to find out what the other states require.

Sources

- Georgia Highway Safety

- Federal Highway Administration

- Bankrate

- National Association of Insurance Commissioners

- LexisNexis Risk Solutions

- AutoInsurance.com

- Insurance Information Institute

- Atlanta Police Department Weekly COBRA Report

- ConsumerAffairs.com

- FRED Economic Data

- Value Penguin

Thanks to John Emil D'Angelo, owner of InsurancePM.com for sharing his expertise.